Payment options are one of the most critical friction points that determine whether an online purchase is completed or abandoned. In Gulf markets, buy-now-pay-later (BNPL) services like Tamara and Tabby have emerged as genuine game-changers. According to Visa's e-commerce report for the Middle East and North Africa, BNPL options contribute to an average order value increase of 30-40%. Meanwhile, DataReportal analysis indicates that GCC e-commerce gross merchandise value crossed $57 billion in 2025, with continued growth projected through 2026.

But integrating these services into your website is not simply a matter of adding a new button to the checkout page. It requires redesigning the entire payment flow, understanding Gulf consumer behavior, and applying UX best practices that reduce cart abandonment and boost conversion rates. At CodeStan, we have implemented BNPL integrations for e-commerce clients across Riyadh, Dubai, and Dammam. Here is what we have learned.

Why BNPL Is Revolutionizing Checkout in the GCC

GCC market dynamics differ from European or North American markets. Gulf consumers are particularly conscious of cash flow management, especially given income diversity and economic fluctuations. BNPL offers a middle ground: receive the product immediately while spreading the cost over comfortable installments.

Key indicators that highlight this shift:

- 82% of GCC e-commerce transactions occur on mobile devices, requiring a seamless payment experience on small screens.

- Pink Media research shows that 58% of online shoppers in Saudi Arabia and the UAE have abandoned a purchase because payment options were unsatisfactory.

- Tamara and Tabby are reshaping online purchasing behavior by offering instant approval experiences that take less than 60 seconds.

- BNPL reduces price sensitivity for higher-ticket items, unlocking categories like electronics, furniture, and travel that previously struggled online.

Understanding Tamara and Tabby

| Capability | Tamara | Tabby |

|---|---|---|

| Primary market | Saudi Arabia | UAE + GCC expansion |

| Approval speed | < 60 seconds | < 60 seconds |

| Arabic RTL checkout | Full support | Full support |

| Mobile SDK | Web + API | iOS, Android, Web |

| Physical retail QR | Limited | Available |

Tamara: The Integrated Saudi Solution

Tamara, backed by Sanabil (the Saudi investment company), offers comprehensive BNPL services tailored for the Saudi market. Its strengths include:

- Seamless integration with local e-commerce platforms like Zid, Salla, and Magento.

- Instant approval based on local data and Saudi credit history (SIMAH).

- Full Arabic language support and RTL-optimized checkout interfaces.

- Regulatory compliance with Saudi Central Bank (SAMA) guidelines.

- Support for both B2C and B2B payment splitting.

Tabby: The UAE-First Cross-Border Player

Tabby originated in the UAE and has expanded across GCC markets. It differentiates through:

- Broader merchant network spanning UAE, Saudi Arabia, Kuwait, and Bahrain.

- Advanced fraud detection using regional behavioral data.

- White-label checkout integration that preserves brand consistency.

- Native app SDKs for iOS and Android alongside web integration.

- Shop Now pay-later options at physical retail points through QR code scanning.

Checkout UX Best Practices for BNPL Integration

1. Display BNPL Early in the Journey

Do not hide BNPL options behind the final checkout step. Our A/B tests for a Dubai electronics retailer showed that displaying "Pay in 4 interest-free installments" on product pages increased add-to-cart rates by 22%. The psychological effect is immediate: a AED 2,400 laptop becomes "AED 600 per month," which feels accessible rather than intimidating.

Recommended placement points:

- Product detail pages, directly below the price

- Mini-cart and full cart summaries

- Checkout step indicators ("Step 2 of 3: Choose Payment Method")

- Email abandoned cart recovery sequences

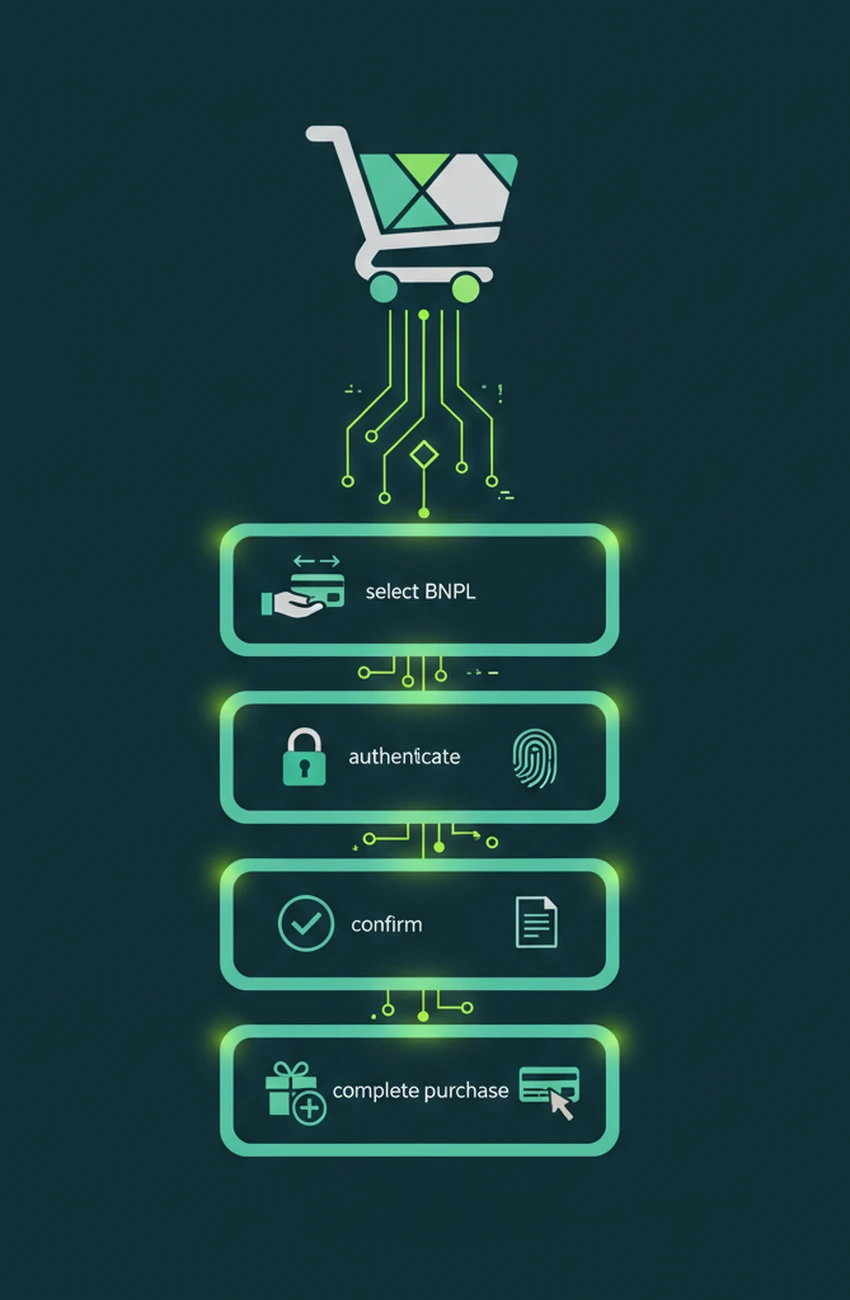

2. Simplify the BNPL Enrollment Flow

Every additional form field reduces completion rates. The most successful BNPL integrations we have built minimize enrollment to three steps:

- Select BNPL: Customer chooses Tamara or Tabby at checkout

- Authenticate: Phone number verification via SMS (no password creation)

- Confirm: Real-time approval and payment schedule display

For a Riyadh fashion brand, reducing the Tabby enrollment from seven steps to three increased BNPL selection rates from 11% to 29% of all checkouts.

3. Design for Mobile-First Checkout

With 82% of transactions on mobile, your BNPL flow must be thumb-friendly and visually clear on 6-inch screens. Key mobile UX principles:

- Payment option buttons must be at least 48px tall with ample spacing

- Use clear visual hierarchy: primary action ("Complete Purchase") above secondary options

- Minimize text input by using address lookup and saved payment methods

- Show progress indicators so users know how many steps remain

- Support biometric authentication (Face ID, fingerprint) where available

4. Build Trust with Transparent Messaging

Gulf consumers are particularly sensitive to hidden fees and ambiguous terms. Every BNPL touchpoint must communicate clearly:

- Exact installment amounts and due dates

- Zero-interest confirmation (if applicable)

- Late fee policies in plain language

- Customer support contact for payment issues

- Regulatory compliance badges (SAMA, UAE Central Bank)

Every additional form field in your BNPL enrollment flow reduces completion rates by approximately 12%. The most successful implementations we have built limit enrollment to three steps: select BNPL, verify phone, confirm schedule.

Technical Integration Considerations

From a development perspective, BNPL integration involves several architectural decisions:

- Webhook handling: Real-time updates for approval, rejection, payment completion, and refunds require robust webhook endpoints with idempotency protection.

- Order state management: Your e-commerce platform must handle edge cases like partial approvals, split payments, and order modifications post-approval.

- Inventory reservation: BNPL approvals can take 10-30 seconds. Implement inventory holds to prevent overselling during this window.

- Multi-currency support: For brands operating across Saudi Arabia (SAR), UAE (AED), and Kuwait (KWD), dynamic currency conversion with BNPL eligibility checks is essential.

- Arabic RTL optimization: Both Tamara and Tabby provide Arabic interfaces, but your checkout must maintain RTL consistency throughout the entire flow.

For a Dammam-based home goods retailer, we built a custom Laravel integration with Tamara that handled 4,000+ BNPL transactions monthly with 99.7% webhook reliability.

Measuring BNPL Impact on Conversion

Track these metrics to evaluate your BNPL implementation:

- BNPL adoption rate: Percentage of checkouts that select BNPL over traditional payment

- Average order value lift: Compare AOV for BNPL orders vs. card/cash orders

- Cart abandonment reduction: Did overall abandonment decrease after BNPL launch?

- Repeat purchase rate: Do BNPL customers return and repurchase?

- Default rate: Monitor late payments to understand customer quality

Key Takeaways

- BNPL increases average order value by 30-40% and reduces cart abandonment in GCC markets

- Tamara excels for Saudi-focused brands; Tabby offers broader GCC coverage

- Display BNPL options early (product pages) rather than hiding them at final checkout

- Limit enrollment to 3 steps maximum; every additional field reduces completion

- Mobile-first design, transparent messaging, and Arabic RTL support are non-negotiable

Want to add BNPL to your GCC store? Get in touch with CodeStan. We have integrated Tamara and Tabby for retailers across Saudi Arabia and the UAE, and we can architect the right solution for your checkout flow.